finance

finance

financeAdaptive Bio-AI Interfaces: Human and Machine Integration

Adaptive Bio-AI InterfacesThe next generation of computing may move beyond screens, keyboards, and touch interfaces toward systems that directly interpret and respond to human biological signals. For decades, human-computer interaction relied on explicit actions such as typing, clicking, speaking, or touching displays. However, advances in neuroscience, biosensors, artificial intelligence, wearable computing, and adaptive machine learning are enabling an entirely different model of interaction.In 2026 and beyond, an emerging concept called Adaptive Bio-AI Interfaces is attracting attention. These systems combine biological data streams with intelligent algorithms that continuously adapt digital experiences based on a person's physiological and cognitive state.Instead of humans learning how to use machines, machines increasingly learn how to understand humans.This evolution could fundamentally transform healthcare, communication, education, productivity, gaming, and human-machine interaction itself.What Are Adaptive Bio-AI Interfaces?Adaptive Bio-AI Interfaces are systems that use biological signals together with artificial intelligence to personalize interactions dynamically.Possible biological inputs include:Brain activity signalsHeart rate patternsEye movement trackingFacial expressionsSkin conductivityMuscle activityRespiration patternsAI systems continuously interpret these signals and modify behavior in real time.Why Human Interfaces Are ChangingTraditional interaction systems have limitations.Manual input requirementsFixed interface designsLimited contextual awarenessCognitive frictionSlow adaptation to user stateFuture systems increasingly seek more natural interaction models.How Adaptive Bio-AI Interfaces WorkThese systems continuously create feedback loops between humans and intelligent systems.Typical process:Biosensors collect physiological signalsAI models interpret patternsContext and behavioral analysis occurInterfaces adapt automaticallyContinuous learning improves responsesThe system evolves alongside the individual user.Core Technologies Behind Bio-AI SystemsArtificial intelligenceBrain-computer interfacesWearable sensorsMachine learning systemsNeural signal processingEdge computing platformsBiometric analysis systemsMultiple technologies converge into a unified interaction ecosystem.Potential ApplicationsAdaptive interfaces may emerge across many sectors.Healthcare monitoring systemsPersonalized education environmentsAdaptive gaming experiencesMental wellness support systemsHuman-robot collaborationAccessibility technologiesWorkplace productivity systemsApplications may extend into nearly every digital environment.Healthcare TransformationHealthcare could become one of the earliest beneficiaries.Continuous patient monitoringNeurological condition detectionStress and fatigue identificationPersonalized treatment systemsRehabilitation supportCare increasingly shifts toward predictive and personalized models.Adaptive Bio-AI Interfaces transform computers from tools that respond to commands into systems that respond to human states.Human Interaction vs Bio-AI InteractionTraditional InterfaceAdaptive Bio-AI InterfaceManual inputBiological signal interpretationStatic experiencesContinuous adaptationUser learns interfaceInterface learns userChallenges and RisksBio-AI systems introduce significant concerns.Biological privacy risksData ownership questionsSecurity vulnerabilitiesAlgorithmic biasBehavior manipulation concernsMental autonomy issuesBiological data may become one of the most sensitive categories of information.Ethical and Governance QuestionsAdaptive systems raise important ethical challenges.Who owns biological data?How should consent operate?Can emotions be manipulated?How much cognitive autonomy should remain?Governance frameworks increasingly become necessary.Future OutlookFuture systems may evolve toward increasingly seamless interaction models.Neural operating systemsEmotion-aware AI assistantsAdaptive digital environmentsHuman-AI cognitive collaborationThe distinction between humans and interfaces may increasingly blur.Frequently Asked QuestionsWhat are Adaptive Bio-AI Interfaces?Systems that combine biological signals with AI to create personalized and adaptive interactions.What biological signals are used?Signals may include brain activity, heart rate, eye movement, facial expressions, and other physiological indicators.Why is this important?Because future systems may become more intuitive, personalized, and responsive to human needs.ConclusionAdaptive Bio-AI Interfaces represent a major evolution in human-computer interaction where machines increasingly adapt themselves to biological and cognitive states. While these technologies promise more personalized experiences and significant advances across healthcare and digital systems, they also raise profound questions regarding privacy, autonomy, ethics, and human identity itself.

Demolishing SWIFT: The Rise of Bilateral CBDC Bridges

Demolishing SWIFT: The Rise of Bilateral CBDC BridgesThe global financial system is entering a period of profound transformation driven by digital currencies, geopolitical shifts, programmable finance, and real-time payment infrastructure. For decades, international money movement relied heavily on centralized messaging networks and correspondent banking systems, with SWIFT functioning as one of the most important components of global financial communication.However, the rise of Central Bank Digital Currencies (CBDCs) introduces a fundamentally different architecture for moving value internationally. Increasingly, governments and central banks are exploring bilateral and regional CBDC bridge systems that could enable direct value transfer between countries without relying on traditional intermediary structures.In 2026 and beyond, this emerging transition is often described as the rise of “Bilateral CBDC Bridges.” While the phrase “Demolishing SWIFT” is provocative, the more realistic discussion involves whether CBDC networks may gradually reduce dependence on existing systems rather than eliminate them entirely.This shift could reshape global payments, international trade, monetary policy, and financial geopolitics.What Is SWIFT?SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a global financial messaging network used by banks and financial institutions.Cross-border payment messagingInterbank communicationTrade settlement instructionsFinancial transaction coordinationSWIFT primarily moves information rather than money itself.Limitations of Traditional International PaymentsConventional international systems often involve multiple intermediaries.Delayed settlement timesHigh transaction costsComplex correspondent banking chainsLimited operating hoursLiquidity requirements across jurisdictionsCross-border transactions can sometimes take days to settle.What Are CBDC Bridges?CBDC bridges are digital infrastructures connecting central bank digital currency systems across jurisdictions.Direct currency exchange mechanismsCross-border settlement systemsShared payment infrastructureProgrammable transaction logicThese systems aim to enable faster movement of value between nations.What Does Bilateral Mean?Bilateral CBDC arrangements involve two countries establishing direct payment connections.Examples could include:Country A digital currency ↔ Country B digital currencyDirect settlement rulesShared compliance standardsIntegrated payment infrastructureTransactions may bypass multiple intermediary institutions.How CBDC Bridges Might WorkFuture systems could operate using shared settlement infrastructure.Digital wallets connect institutionsTransaction requests are validatedCurrency conversion occurs automaticallySettlement executes instantlyValue transfer becomes increasingly direct.Potential BenefitsNear real-time settlementReduced transaction costsLower dependency on intermediariesImproved liquidity efficiency24/7 operational capabilityPayment infrastructure may become significantly faster and more efficient.Geopolitical ImplicationsCBDC bridges are not purely technological developments.Monetary sovereignty concernsInternational trade relationshipsFinancial influence shiftsStrategic payment independencePayment infrastructure increasingly intersects with geopolitics.The future question may not be whether SWIFT disappears, but whether global payments evolve from centralized messaging systems toward interconnected digital settlement networks.SWIFT vs Bilateral CBDC BridgesSWIFT ModelCBDC Bridge ModelMessaging-focusedSettlement-focusedMultiple intermediariesDirect connectionsDelayed settlementPotential near real-time settlementTraditional infrastructureDigital-native systemsChallenges and RisksCBDC bridge systems face significant hurdles.Interoperability issuesCybersecurity threatsPrivacy concernsRegulatory fragmentationPolitical coordination difficultiesTechnical standardization challengesGlobal payment systems require high levels of trust and coordination.Possible Future ScenariosSWIFT integrates with CBDC systemsRegional CBDC networks emergeHybrid international payment systems developDirect bilateral settlement ecosystems expandA mixed infrastructure model appears more likely than an immediate replacement.Economic and Strategic ImplicationsThe growth of bilateral CBDC bridges could reshape global finance.Changes in international payment economicsReduced settlement frictionNew monetary relationshipsEvolution of digital trade ecosystemsThe architecture of global money movement may increasingly shift toward programmable and interconnected systems.Frequently Asked QuestionsWill CBDCs replace SWIFT?Near term, a coexistence model appears more likely than complete replacement.What is a CBDC bridge?A system connecting multiple central bank digital currencies for cross-border settlement.Why are countries interested in bilateral CBDC systems?Potential reasons include faster payments, reduced costs, and greater financial independence.Conclusion“Demolishing SWIFT” is a dramatic framing, but the broader reality involves a gradual redesign of international financial infrastructure. Bilateral CBDC bridges represent a move toward programmable, direct, and digital-native settlement systems that could reduce reliance on traditional intermediary structures. Rather than eliminating existing systems overnight, the future may involve interconnected layers where legacy infrastructure and digital currency networks operate together.

The Machine Fiduciary Dilemma in AI-Driven Finance

The "Machine Fiduciary" DilemmaThe global financial system is entering a phase where artificial intelligence is no longer functioning merely as an analytical assistant but increasingly acts as an autonomous decision-maker. AI systems already assist with portfolio management, lending decisions, fraud detection, insurance underwriting, treasury optimization, and personalized financial recommendations.As these systems become more sophisticated, financial institutions increasingly explore whether AI agents can move beyond advice and begin directly representing human interests.Historically, fiduciary obligations belonged to human professionals such as trustees, financial advisors, investment managers, lawyers, and corporate directors. Their legal and ethical obligation was clear: act in the best interests of those they represent.The emergence of autonomous AI creates a difficult question:Can machines responsibly exercise duties that traditionally required human judgment, ethics, and accountability?This question forms the basis of what many describe as the "Machine Fiduciary" Dilemma.What Is a Fiduciary?A fiduciary is a person or institution legally required to place another party's interests above their own.Investment advisorsTrust managersCorporate board membersEstate administratorsLegal representativesTraditional fiduciary responsibility includes:Duty of loyaltyDuty of careConflict avoidanceTransparency requirementsResponsible decision-makingThese obligations assume human reasoning and accountability.What Is a Machine Fiduciary?A machine fiduciary refers to an AI system authorized to make decisions on behalf of individuals or organizations while attempting to act in their best interests.Potential examples include:AI portfolio managersAutonomous retirement plannersAI trust administratorsCorporate treasury agentsAutonomous contract negotiatorsThe machine moves from assistant to delegated representative.Why the Dilemma ExistsAI systems optimize based on measurable objectives. Human fiduciary duties often involve ambiguous and competing priorities.Examples include:Short-term profits versus long-term wellbeingRisk versus opportunityIndividual interests versus collective outcomesFinancial efficiency versus ethical concernsMathematical optimization does not automatically equal responsible judgment.Possible Advantages of Machine FiduciariesSupporters argue that AI systems may improve financial decision-making.Continuous monitoringFaster information processingLower operational costsPersonalized optimizationReduced emotional bias24/7 availabilityMachines may provide highly consistent and scalable decision support.Potential Real-World ApplicationsMachine fiduciaries could potentially emerge in multiple sectors.Personal finance managementRetirement planning systemsHealthcare resource allocationCorporate treasury managementInsurance decision systemsLegal and trust administrationAutonomous representation may extend far beyond investing.The Accountability ProblemThe largest challenge involves responsibility.If an AI acting as a fiduciary creates harm, several difficult questions emerge:Is the developer responsible?Is the institution responsible?Is the user responsible?Is the regulator responsible?Can responsibility be assigned to AI itself?Existing legal systems generally assume accountable human actors.The Machine Fiduciary Dilemma is not primarily a technology problem—it is a trust and responsibility problem.Human Fiduciaries vs Machine FiduciariesHuman FiduciaryMachine FiduciaryContextual judgmentData optimizationEthical reasoningRule executionLegal accountabilityUnclear accountabilityEmotional understandingPattern analysisFuture systems may combine strengths from both models.AI Alignment ChallengesMachine fiduciaries may struggle with understanding human intentions accurately.Ambiguous objectivesConflicting valuesPreference uncertaintyGoal misalignmentUnexpected optimization outcomesDefining “best interests” may prove difficult.Governance and Regulatory QuestionsFuture AI fiduciary systems may require new legal structures.Human oversight requirementsExplainability standardsAudit trailsAI liability frameworksOverride mechanismsGovernance may become essential infrastructure.Future OutlookRather than fully replacing humans, machine fiduciaries may initially emerge as collaborative systems.Human-AI co-decision systemsAutonomous financial co-pilotsAdaptive trust frameworksAI-assisted fiduciary governanceThe future may involve machines enhancing fiduciary decisions rather than independently controlling them.Frequently Asked QuestionsWhat is a machine fiduciary?An AI system authorized to make decisions while representing another party's interests.Why is it considered a dilemma?Because fiduciary responsibility requires trust, ethics, judgment, and accountability—areas where AI raises difficult questions.Will AI replace financial advisors?Near-term systems are more likely to augment and support human professionals rather than fully replace them.ConclusionThe Machine Fiduciary Dilemma represents one of the most important governance questions of the AI economy. As AI increasingly gains authority to act rather than merely advise, society must determine how trust, accountability, ethics, and responsibility should evolve. The challenge is no longer whether machines can make decisions; the challenge is deciding how much responsibility humans are willing to delegate.

Synthetic Identity Bank Runs and Financial Security Threats

Synthetic Identity Bank RunsThe digital financial system increasingly depends on identity as a foundational layer for trust, lending, payments, onboarding, and risk management. Historically, banking systems assumed that identities represented genuine individuals or legally verified entities. However, advances in artificial intelligence, large-scale data aggregation, deepfake technology, automated account creation systems, and synthetic identity generation are introducing entirely new categories of financial risk.In 2026 and beyond, analysts increasingly discuss a potential future phenomenon called “Synthetic Identity Bank Runs,” where large-scale AI-generated or fabricated identities could simultaneously create liquidity pressure, fraud exposure, or operational stress across financial institutions.This concept extends beyond traditional fraud and enters the realm of systemic financial risk.What Is a Synthetic Identity?A synthetic identity is an artificially constructed identity created by combining real and fabricated information.Generated personal informationPartially real identity elementsAI-generated documentationFabricated digital behavior patternsArtificial account historiesSynthetic identities may not correspond to real individuals.What Is a Synthetic Identity Bank Run?A synthetic identity bank run describes a scenario where large-scale fabricated identities create coordinated pressure on financial systems.Mass account creationFraudulent credit extractionArtificial deposit flowsAutomated withdrawal activityLiquidity stress amplificationThe threat emerges from scale and automation rather than isolated fraud events.How Traditional Bank Runs WorkTraditional bank runs occur when customers lose confidence and rapidly withdraw funds.Fear-driven withdrawal behaviorLiquidity shortagesLoss of confidenceContagion effectsPsychology historically played the central role.How Synthetic Identity Runs Could DifferFuture synthetic scenarios may emerge from algorithmic activity rather than human behavior.AI-driven account generationMachine-executed financial actionsCoordinated digital activityHigh-speed systemic interactionsAlgorithms could potentially create financial stress faster than humans.Technologies Potentially Enabling Synthetic Identity RisksArtificial intelligenceDeepfake generation systemsLarge language modelsAutomated bot ecosystemsIdentity fabrication softwareTechnological progress increases both capability and complexity.Potential Attack PathwaysMultiple pathways could theoretically create systemic pressure.Fraudulent loan applicationsMass payment network manipulationArtificial credit expansionDeposit instability eventsSynthetic customer ecosystemsSystem interconnectedness increases potential impact.Why Scale MattersIndividual fraud cases typically create limited financial damage. Systemic risk emerges when activities scale dramatically.Millions of automated identitiesHigh-frequency transaction activityCross-platform coordinationRapid propagation effectsAutomation compresses the timeline of potential disruption.AI and Defensive Risk IntelligenceArtificial intelligence increasingly helps defend financial systems.Behavioral anomaly detectionIdentity verification intelligenceTransaction network analysisFraud prediction systemsAI increasingly becomes both the challenge and the defense.Benefits of Advanced Identity SystemsReduced fraud exposureStronger authentication systemsImproved financial trustGreater cybersecurity resilienceEnhanced customer protectionIdentity innovation strengthens financial infrastructure.Future financial stability may depend as much on identity integrity as on capital and liquidity management.Traditional Fraud vs Synthetic Identity RiskTraditional → Human-operated fraud schemesSynthetic → AI-generated scalable ecosystemsTraditional → Individual incidentsSynthetic → Potential systemic effectsThe scale and speed of risk dynamics may change significantly.Digital Identity and Verification SystemsFuture banking ecosystems increasingly require stronger identity infrastructure.Biometric authenticationCryptographic identity systemsBehavioral verification modelsZero-knowledge proof frameworksTrust increasingly becomes technologically enforced.Regulatory and Governance ChallengesGovernments and financial institutions increasingly face new requirements.Identity standardsAI accountability frameworksCross-border verification systemsFraud monitoring regulationsGovernance becomes increasingly important.Future of Financial Identity SystemsFuture ecosystems may evolve toward highly intelligent identity networks.Self-sovereign identitiesContinuous authentication systemsAI-native trust infrastructureAdaptive financial identity ecosystemsIdentity increasingly becomes core financial infrastructure.Economic and Strategic ImplicationsSynthetic identity risks could reshape the future architecture of finance.Expansion of cybersecurity investmentsTransformation of onboarding systemsEvolution of fraud intelligenceRedesign of digital trust infrastructureThis evolution may fundamentally redefine how financial systems establish trust in the digital era.Frequently Asked QuestionsWhat is a synthetic identity?An artificially created identity combining fabricated and real information.What is a synthetic identity bank run?A theoretical scenario where large-scale AI-generated identities create financial stress through coordinated activity.Why is this important?Because identity integrity increasingly underpins digital finance, payments, and banking systems.ConclusionSynthetic Identity Bank Runs represent a future-oriented concept highlighting how AI-generated identities and automated systems could create new categories of systemic financial risk. While this remains largely theoretical, the broader trend is real: financial systems increasingly depend on digital trust infrastructure. As artificial intelligence advances, future resilience may require stronger identity frameworks, continuous verification systems, and adaptive cybersecurity defenses.

Parametric Micro-Hedging for Small Business Risk Protection

Parametric Micro-Hedging for Small BusinessesSmall businesses increasingly operate in an environment characterized by climate uncertainty, supply-chain disruptions, fluctuating commodity prices, changing customer behavior, cyber threats, and macroeconomic volatility. Traditionally, risk management and hedging strategies were largely reserved for large corporations with sophisticated treasury teams and access to derivatives markets.In 2026, an emerging financial concept known as “Parametric Micro-Hedging” is attracting attention as a potential solution for smaller enterprises. This model combines AI-driven risk intelligence, real-time data feeds, automated insurance structures, and programmable financial contracts to provide highly targeted protection against specific business risks.Instead of requiring large hedging positions or complex financial products, micro-hedging enables small businesses to obtain precise and affordable risk coverage.This evolution could fundamentally transform financial resilience for small enterprises.What Is Hedging?Hedging is a strategy used to reduce financial exposure to uncertainty or adverse events.Price volatility protectionRevenue stabilizationRisk transfer mechanismsFinancial uncertainty reductionThe objective is not eliminating risk entirely, but limiting its impact.What Is Parametric Micro-Hedging?Parametric micro-hedging refers to automated financial protection triggered by predefined measurable events.Weather-based triggersSupply-chain event triggersSales decline thresholdsCommodity price movementsOperational disruption indicatorsPayments occur automatically when specific conditions are met.What Makes It “Parametric”?Traditional insurance often depends on assessing actual losses after an event occurs. Parametric systems instead rely on predefined measurable conditions.Examples include:Rainfall exceeding specified levelsTemperature thresholdsShipping delays beyond certain limitsCommodity prices reaching trigger pointsCompensation becomes event-driven rather than claim-driven.How Parametric Micro-Hedging WorksModern systems continuously monitor business conditions and environmental signals.Real-time data collectionRisk monitoring systemsAI prediction modelsAutomated payout executionRisk protection increasingly becomes automated and continuous.Examples of Small Business Use CasesMicro-hedging may support many business types.Restaurants protecting against weather disruptionsRetail businesses hedging inventory delaysAgricultural firms protecting crop revenueLogistics companies managing fuel volatilityLocal businesses protecting against demand shocksProtection becomes highly specific to business operations.Technologies Driving Micro-HedgingArtificial intelligenceInternet of Things (IoT)Real-time analytics platformsSmart contractsBlockchain settlement systemsTechnology reduces cost and increases accessibility.Benefits of Parametric Micro-HedgingLower protection costsFaster payoutsReduced paperworkGreater financial resilienceImproved cash-flow stabilitySmall businesses gain access to sophisticated financial protection mechanisms.Parametric micro-hedging transforms risk management from expensive institutional infrastructure into accessible, automated protection for small businesses.Traditional Insurance vs Parametric Micro-HedgingTraditional → Manual claims assessmentMicro-Hedging → Automatic trigger-based payoutsTraditional → Broad risk categoriesMicro-Hedging → Highly targeted risk coverageThis changes how business protection systems operate.AI and Predictive Risk IntelligenceArtificial intelligence increasingly powers risk systems.Demand forecastingWeather prediction systemsSupply-chain disruption analysisBusiness trend detectionAI strengthens proactive protection capabilities.Challenges and RisksMicro-hedging systems also introduce important challenges.Incorrect trigger calibrationData quality issuesAlgorithmic biasCoverage gapsTechnology dependenceCareful design and monitoring remain essential.Regulatory ConsiderationsFinancial regulators increasingly evaluate automated protection systems.Consumer protection requirementsSmart contract oversightData governance standardsRisk disclosure obligationsRegulatory frameworks continue evolving.Future of Small Business Risk ManagementThe future may involve highly personalized and automated financial protection ecosystems.AI-native risk platformsContinuous business monitoringAutonomous protection systemsIntegrated financial resilience networksRisk management increasingly becomes embedded infrastructure.Economic and Strategic ImplicationsThe rise of parametric micro-hedging could reshape financial resilience for smaller enterprises.Expansion of small-business financial toolsReduced operational vulnerabilityImproved economic resilienceDemocratization of risk-management capabilitiesThis evolution may fundamentally change how small businesses protect themselves from uncertainty.Frequently Asked QuestionsWhat is parametric micro-hedging?A targeted risk-protection system where predefined events automatically trigger financial payouts.Why is it useful for small businesses?Because it offers affordable and automated protection against specific risks.What triggers payouts?Specific measurable events such as weather conditions, supply-chain disruptions, or price changes.ConclusionParametric Micro-Hedging for Small Businesses represents a major evolution in financial protection where AI, predictive analytics, and programmable contracts make sophisticated risk management more accessible. By transforming risk coverage into automated and event-driven systems, small enterprises may gain stronger resilience against increasingly unpredictable business environments. While operational and regulatory challenges remain, these systems could become foundational infrastructure for the future of small-business finance.

The Gray Wave Portfolio Restructure: Aging Wealth Trends

The "Gray Wave" Portfolio RestructureThe global economy is entering a demographic transformation unlike any seen in modern financial history. Populations across many countries are aging rapidly due to declining birth rates, longer life expectancy, and improvements in healthcare systems. This demographic transition—often referred to as the “Gray Wave”—is not simply a social trend; it is increasingly becoming a major force reshaping capital markets, investment strategies, labor economics, and institutional portfolio management.In 2026 and beyond, investors, pension funds, insurance firms, sovereign wealth funds, and asset managers are increasingly adapting to what many analysts describe as the “Gray Wave Portfolio Restructure.” This involves adjusting investment allocations and financial strategies to account for aging populations and changing economic behaviors.This evolution could fundamentally transform long-term capital allocation and the future structure of global financial markets.What Is the Gray Wave?The Gray Wave refers to large-scale demographic aging across populations.Longer life expectancyLower birth ratesGrowing retiree populationsChanging workforce structuresDemographic change increasingly becomes an economic force.What Is a Gray Wave Portfolio Restructure?Gray Wave Portfolio Restructure refers to changes in investment strategies driven by demographic aging patterns.Adjustments in asset allocationIncome-focused investment modelsLongevity risk managementHealthcare and retirement exposure strategiesPortfolios increasingly adapt to demographic realities.Why Demographics Matter to MarketsPopulation structures influence economic behavior and capital flows.Consumption pattern shiftsRetirement savings dynamicsHealthcare spending growthLabor market changesLong-term investment behaviorDemographics increasingly shape economic outcomes.How Portfolios May ChangeAsset managers increasingly adjust exposure to sectors influenced by aging populations.Healthcare and biotechnology investmentsRetirement income assetsInfrastructure supporting elderly populationsLong-duration income strategiesInvestment priorities shift toward demographic resilience.Sectors Potentially Benefiting from the Gray WaveSeveral industries may experience increased demand.Healthcare technologyBiotechnology and longevity researchSenior housing infrastructureRetirement financial productsMedical devices and digital healthDemographic trends create long-term investment themes.Impact on Pension SystemsAging populations create challenges for retirement systems.Higher retirement obligationsLonger payout periodsFunding pressureAsset-liability matching complexityPension institutions increasingly require portfolio redesign.AI and Demographic IntelligenceArtificial intelligence increasingly supports demographic investment analysis.Population trend forecastingBehavioral spending predictionLongevity modelingDynamic asset allocation systemsAI strengthens long-term investment planning.Benefits of Demographic-Aware Portfolio StrategiesBetter long-term risk managementImproved income planningEnhanced sector allocationGreater resilience to structural economic shiftsLong-term capital optimizationDemographic intelligence increasingly becomes an investment advantage.The Gray Wave transforms demographics from population statistics into one of the most influential forces shaping future capital markets.Traditional Portfolio Models vs Gray Wave StrategiesTraditional → Economic-cycle focused allocationsGray Wave → Demographic-driven allocationsTraditional → Broad market assumptionsGray Wave → Population trend intelligenceThis changes how long-term investment strategies are built.Risks and ChallengesDemographic restructuring introduces uncertainties.Economic growth slowdown risksLabor shortagesHealthcare cost expansionRetirement funding pressureGovernment fiscal stressPopulation trends can create broad economic consequences.Geopolitical ImplicationsDifferent demographic patterns may reshape global competition.Regional workforce shiftsMigration policy changesHealthcare infrastructure demandChanges in economic growth leadershipDemographics increasingly influence geopolitical dynamics.Future of Gray Wave InvestingFuture investment systems may become increasingly demographic-aware.AI-native demographic investingLongevity-linked financial productsPersonalized retirement ecosystemsAdaptive long-term portfolio systemsInvestment strategies increasingly incorporate population intelligence.Economic and Strategic ImplicationsThe Gray Wave Portfolio Restructure could reshape global capital allocation.Transformation of investment prioritiesExpansion of healthcare economiesEvolution of retirement systemsLong-term restructuring of financial marketsThis demographic transition may become one of the defining economic forces of the coming decades.Frequently Asked QuestionsWhat is the Gray Wave?A demographic trend involving aging populations and growing retiree segments.What is Gray Wave Portfolio Restructure?Investment strategy adjustments designed to account for demographic aging patterns.Why does aging affect financial markets?Because demographics influence spending patterns, labor markets, savings behavior, and long-term capital allocation.ConclusionThe Gray Wave Portfolio Restructure represents a significant shift in how investors and institutions may approach long-term capital allocation. As aging populations reshape economic structures and consumption patterns, investment systems increasingly adapt to demographic realities. While this transformation introduces challenges related to pensions, healthcare costs, and growth dynamics, it also creates opportunities for innovation, sector evolution, and more sophisticated investment strategies.

Algorithmic Collateral Cleansing in Modern Financial Systems

Algorithmic Collateral CleansingFinancial markets are entering an era where artificial intelligence, real-time risk systems, digital assets, and automated treasury infrastructure increasingly influence how institutions manage balance sheets and capital efficiency. Traditionally, collateral management depended heavily on periodic reviews, manual risk assessments, and static valuation frameworks. However, modern financial ecosystems increasingly require dynamic and continuous optimization.In 2026 and beyond, an emerging concept gaining attention is “Algorithmic Collateral Cleansing.” This model uses AI systems, predictive analytics, and automated financial intelligence to continuously evaluate, replace, optimize, and remove inefficient or deteriorating collateral from financial systems.This evolution could fundamentally transform liquidity management, capital efficiency, systemic risk monitoring, and institutional treasury operations.What Is Collateral?Collateral refers to assets pledged to secure financial obligations or reduce risk exposure.Government securitiesCorporate bondsCash reservesReal estate assetsTokenized financial assetsCollateral functions as a protective mechanism within financial systems.What Is Algorithmic Collateral Cleansing?Algorithmic collateral cleansing refers to automated systems that continuously identify inefficient, deteriorating, or risky collateral and optimize asset quality across financial portfolios.Automated collateral quality scoringDynamic asset replacement systemsReal-time risk monitoringAI-powered portfolio optimizationCollateral management shifts from periodic review toward continuous intelligence.Why Traditional Collateral Systems Are ChangingConventional collateral frameworks face several operational limitations.Manual review processesDelayed risk identificationStatic asset valuationsLiquidity inefficienciesFragmented monitoring systemsModern financial systems increasingly require real-time adaptability.How Algorithmic Collateral Cleansing WorksIntelligent systems continuously monitor and optimize collateral portfolios.Real-time market data collectionAsset risk scoringPredictive deterioration analysisAutomatic collateral substitutionOptimization increasingly occurs without manual intervention.Technologies Driving Collateral IntelligenceArtificial intelligenceMachine learning risk modelsPredictive analytics systemsBlockchain settlement infrastructureReal-time market intelligence platformsTechnology increasingly enables autonomous treasury operations.Examples of Collateral Cleansing ActivitiesAutomated systems may perform multiple optimization actions.Replacing deteriorating assetsRemoving low-liquidity securitiesAdjusting collateral allocation dynamicallyOptimizing exposure across counterpartiesAsset quality becomes continuously managed.Benefits of Algorithmic Collateral SystemsImproved capital efficiencyReduced operational complexityEnhanced liquidity managementEarlier risk detectionBetter balance sheet optimizationAutomation may significantly improve institutional financial performance.Algorithmic collateral cleansing transforms collateral from static balance-sheet assets into continuously optimized financial intelligence systems.Traditional Collateral Management vs Algorithmic CleansingTraditional → Periodic manual reviewsAlgorithmic → Continuous real-time optimizationTraditional → Static collateral assignmentsAlgorithmic → Dynamic intelligent allocationThis transition changes how financial institutions manage risk.AI and Predictive Risk IntelligenceArtificial intelligence increasingly supports collateral decisions.Market stress predictionCredit deterioration analysisLiquidity forecasting systemsDynamic exposure managementAI improves speed and predictive capabilities.Tokenized Collateral EcosystemsDigital assets may further transform collateral systems.Tokenized securitiesProgrammable collateral contractsInstant settlement systemsFractional collateral ownershipCollateral increasingly becomes digitally native.Risks and ChallengesAlgorithmic collateral systems introduce important concerns.Model errors and biasOver-automation risksCybersecurity vulnerabilitiesMarket concentration effectsSystemic feedback loopsHuman oversight remains important.Regulatory ConsiderationsRegulators increasingly examine AI-based treasury systems.Algorithm transparency requirementsStress testing frameworksRisk governance standardsFinancial stability oversightGovernance systems remain critical for adoption.Future of Collateral IntelligenceThe future financial ecosystem may increasingly rely on autonomous optimization systems.AI-native treasury operationsContinuous balance-sheet intelligencePredictive liquidity ecosystemsAutonomous capital managementFinancial systems increasingly move toward real-time intelligence.Economic and Strategic ImplicationsThe rise of algorithmic collateral systems could reshape global financial infrastructure.Transformation of treasury economicsGreater market efficiencyEnhanced liquidity resilienceEvolution of institutional financial operationsThis transition may fundamentally change how financial assets are managed across future economies.Frequently Asked QuestionsWhat is algorithmic collateral cleansing?An AI-driven process that continuously evaluates and optimizes collateral quality.Why is it important?Because it can improve liquidity efficiency, reduce risk exposure, and optimize capital allocation.What risks exist?Potential risks include algorithmic failures, systemic feedback effects, and excessive automation dependence.ConclusionAlgorithmic Collateral Cleansing represents a future evolution in financial infrastructure where collateral becomes continuously monitored and optimized through intelligent systems. By combining AI, predictive analytics, real-time market data, and digital financial infrastructure, institutions may create more resilient and efficient capital ecosystems. While significant operational and governance challenges remain, this approach could become a foundational capability for next-generation treasury and risk management systems.

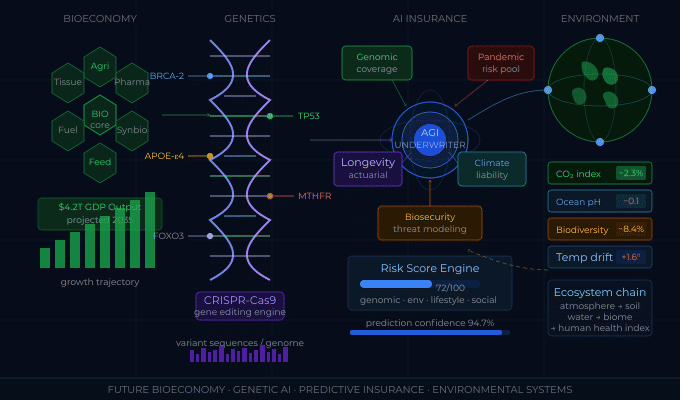

Future bioeconomy genetic technology AI insurance environmental systems concept

"De-Extinction" Underwriting & Bio-Risk PremiumThe convergence of synthetic biology, gene editing, biodiversity engineering, and de-extinction technologies is creating entirely new categories of economic risk. For decades, insurance and underwriting systems focused primarily on familiar domains such as property damage, health events, environmental risks, and financial uncertainty. However, advances in biotechnology are introducing risks associated with engineered ecosystems, revived species, synthetic organisms, and large-scale biological interventions.In 2026 and beyond, a new concept is emerging: “De-Extinction Underwriting” and the rise of Bio-Risk Premium models. These frameworks attempt to quantify and price risks associated with resurrected species, engineered biological systems, ecosystem disruption, and synthetic life technologies.This evolution could fundamentally transform insurance, environmental risk assessment, and the economics of biotechnology.What Is De-Extinction?De-extinction refers to scientific efforts aimed at restoring extinct species or creating functionally similar organisms using modern biotechnology.Genetic reconstruction techniquesGene-editing systemsSynthetic biology platformsSelective breeding technologiesBiological ecosystem engineeringThe objective is not simply recreating ancient organisms but potentially restoring ecological functions.What Is De-Extinction Underwriting?De-extinction underwriting refers to risk assessment frameworks used to evaluate and price biological uncertainties associated with revived or engineered species.Ecosystem disruption analysisSpecies behavior predictionBiological containment assessmentLong-term environmental impact modelingInsurance systems increasingly adapt to biological complexity.What Is a Bio-Risk Premium?A bio-risk premium represents additional financial costs or pricing adjustments reflecting uncertainty associated with biological technologies.Environmental uncertainty premiumsGenetic risk adjustmentsContainment risk pricingEcosystem volatility factorsBiological uncertainty becomes measurable financial risk.Why Traditional Risk Models Are ChangingConventional insurance frameworks were not designed for synthetic biological systems.Limited historical datasetsUnpredictable ecosystem interactionsNovel biological behavior patternsCross-disciplinary risk complexityBiotechnology introduces new categories of uncertainty.Potential Bio-Risks in De-Extinction ProgramsSeveral risks could emerge from large-scale biological engineering projects.Unexpected ecosystem disruptionSpecies adaptation failuresDisease transmission pathwaysGenetic instability risksBiodiversity imbalance effectsComplex biological systems can create difficult-to-predict outcomes.AI and Bio-Risk ModelingArtificial intelligence increasingly supports biological forecasting systems.Predictive ecosystem simulationBehavioral pattern modelingGenetic interaction analysisRisk scenario forecastingAI expands the ability to analyze biological complexity.Applications of Bio-Risk UnderwritingFuture insurance and financial systems may apply these models broadly.Biotechnology companiesEnvironmental restoration projectsAgricultural genetic systemsSynthetic biology laboratoriesConservation initiativesRisk frameworks increasingly extend into biological innovation.Benefits of Bio-Risk Intelligence SystemsImproved risk visibilityEnhanced environmental forecastingGreater investor confidenceMore informed biotechnology decisionsImproved ecosystem managementAdvanced risk intelligence may improve responsible innovation.As biotechnology expands beyond traditional boundaries, biological uncertainty itself becomes a measurable financial and strategic variable.Traditional Underwriting vs Bio-Risk UnderwritingTraditional → Historical event-based modelsBio-Risk → Predictive ecosystem intelligenceTraditional → Static actuarial frameworksBio-Risk → Dynamic biological simulationsThis transition changes how uncertainty is measured.Ethical and Governance ChallengesBiological engineering introduces difficult ethical questions.Species welfare concernsEcological intervention ethicsLong-term environmental responsibilityOwnership of engineered organismsTechnology alone cannot resolve these challenges.Regulatory ConsiderationsGovernments and scientific organizations may require new frameworks.Biological safety standardsContainment requirementsEnvironmental assessment regulationsCross-border biotechnology governanceRegulation becomes critical for responsible deployment.Future of Bio-Risk EconomicsThe future bioeconomy may increasingly rely on sophisticated risk systems.AI-native biological forecastingDynamic ecosystem insuranceProgrammable environmental risk systemsIntegrated biotechnology financial modelsRisk analysis increasingly becomes a component of biological innovation.Economic and Strategic ImplicationsBio-risk frameworks could reshape biotechnology economics.Expansion of biotech insurance marketsNew investment evaluation modelsGrowth of biological risk intelligence systemsTransformation of environmental financeThis evolution may redefine how society evaluates uncertainty in future biological systems.Frequently Asked QuestionsWhat is de-extinction underwriting?A framework used to assess and price risks associated with revived or engineered biological systems.What is a bio-risk premium?An additional risk cost reflecting uncertainty associated with biological technologies and ecosystem effects.Why is this important?Because emerging biotechnology may create risks that traditional financial and insurance systems are not designed to evaluate.ConclusionDe-Extinction Underwriting and Bio-Risk Premium models represent a future where biotechnology and finance increasingly intersect. As synthetic biology, ecosystem engineering, and species restoration efforts expand, risk systems may evolve beyond conventional actuarial methods into predictive biological intelligence platforms. While these developments could support responsible innovation and environmental restoration, they also introduce profound scientific, ethical, regulatory, and economic challenges that may shape the future bioeconomy.

The GPU-Compute Commodity Market: AI Infrastructure Economy

The GPU-Compute Commodity MarketThe global economy is entering an era where computational power is becoming as strategically valuable as energy, oil, and telecommunications infrastructure. Artificial intelligence, machine learning, large language models, robotics, scientific simulations, and cloud-native applications increasingly depend on specialized computational hardware—particularly Graphics Processing Units (GPUs).In 2026, a major emerging trend is the evolution of GPU resources from infrastructure components into a tradable economic asset class. This development is giving rise to what many analysts describe as the “GPU-Compute Commodity Market,” where computing capacity itself becomes a liquid market with pricing mechanisms, trading systems, futures contracts, and dynamic supply-demand economics.This transformation may fundamentally reshape cloud economics, AI development, digital infrastructure, and global technology markets.What Is a GPU-Compute Commodity Market?A GPU-compute commodity market is an economic ecosystem where computational resources can be bought, sold, reserved, exchanged, or traded similarly to traditional commodities.GPU capacity tradingFuture compute reservationsDynamic market pricingComputational resource exchangesCompute itself becomes a measurable and tradable economic unit.Why GPUs Are Becoming Strategic AssetsSeveral factors are dramatically increasing GPU demand.Large AI model trainingGrowth of AI agentsExpansion of inference workloadsScientific research computingAutonomous systems and roboticsDemand for specialized computation increasingly exceeds available supply.Why Traditional Cloud Models Are ChangingTraditional cloud allocation methods face several limitations.Fixed pricing structuresResource shortagesLong-term reservation inefficienciesLimited flexibility in allocationSupply-demand mismatchesOrganizations increasingly require dynamic access to computational resources.How GPU Commodity Markets Might WorkFuture compute markets may operate similarly to traditional commodity exchanges.Providers supply compute inventoryBuyers reserve future compute accessMarkets determine pricing dynamicallyParticipants trade resource contractsComputational capacity becomes continuously priced infrastructure.Potential ParticipantsMultiple industries could participate in GPU marketplaces.Cloud service providersAI development companiesFinancial institutionsSemiconductor firmsEnterprise technology organizationsCompute ecosystems could become highly interconnected.Benefits of Compute Commodity MarketsImproved allocation efficiencyBetter price discoveryReduced resource wasteGreater liquidity and flexibilityEnhanced infrastructure planningDynamic markets may improve compute accessibility.Compute Futures and DerivativesGPU markets may introduce sophisticated financial products.Compute futures contractsCapacity reservation agreementsOptions linked to GPU availabilityRisk management instrumentsCompute may evolve into a full financial asset class.As AI becomes foundational infrastructure, computational power increasingly resembles a strategic commodity rather than a simple technical resource.Traditional Cloud Infrastructure vs GPU Commodity MarketsTraditional → Fixed resource allocationCommodity Market → Dynamic supply-demand pricingTraditional → Static pricing modelsCommodity Market → Real-time market valuationThis transition changes how computational resources are acquired and managed.AI and Autonomous Resource AllocationArtificial intelligence may increasingly manage compute ecosystems.Demand forecasting systemsAutomated pricing optimizationDynamic infrastructure balancingPredictive resource allocationAI increasingly coordinates AI infrastructure itself.Role of TokenizationBlockchain systems may support tradable compute markets.Tokenized compute ownershipSmart contract settlementsProgrammable resource exchangesFractional compute participationDigital infrastructure increasingly intersects with financial systems.Challenges and RisksGPU commodity markets introduce several important risks.Market speculation risksResource concentration concernsPrice volatilityInfrastructure monopolization risksRegulatory uncertaintyGovernance frameworks remain essential.Geopolitical ImplicationsGPU access increasingly influences national competitiveness.Semiconductor supply chain competitionNational AI strategiesTechnology export controlsDigital sovereignty initiativesComputation increasingly becomes a strategic national asset.Future of Compute MarketsFuture computational economies may become increasingly sophisticated.Global compute exchangesAI-managed infrastructure marketsContinuous resource auctionsMachine-driven compute negotiationsCompute markets may become a foundational component of future digital economies.Economic and Strategic ImplicationsThe rise of GPU commodity markets could reshape digital infrastructure economics.New infrastructure financing modelsExpansion of digital asset classesAcceleration of AI innovationTransformation of cloud business modelsThis evolution may fundamentally change how computational resources are valued and distributed globally.Frequently Asked QuestionsWhat is a GPU-compute commodity market?A market where computational resources are traded similarly to traditional commodities.Why are GPUs becoming strategic?Because AI systems increasingly require enormous computational resources for training and inference.What risks exist in GPU markets?Potential risks include speculation, resource concentration, and infrastructure volatility.ConclusionThe GPU-Compute Commodity Market represents a major transformation in digital infrastructure economics by turning computational capacity into a strategic and potentially tradable asset. As AI demand continues expanding, compute resources may increasingly resemble energy or telecommunications infrastructure, supported by dynamic pricing systems, financial instruments, and global marketplaces. While such markets promise greater efficiency and flexibility, they also introduce important challenges related to fairness, concentration, regulation, and geopolitical competition.

Zero-Click Insurance and Predictive Macro-Claims Explained

"Zero-Click" Insurance & Predictive Macro-ClaimsThe insurance industry is moving through one of its largest transformations since the introduction of digital underwriting. Historically, insurance has depended heavily on customer actions such as filling out applications, submitting documents, filing claims, and interacting with human agents. However, the convergence of artificial intelligence, real-time sensor networks, behavioral analytics, connected devices, and predictive modeling is creating a radically different insurance ecosystem.In 2026, an emerging concept gaining attention is “Zero-Click Insurance” combined with “Predictive Macro-Claims.” Instead of requiring customers to manually initiate coverage events or submit claims, intelligent systems increasingly anticipate risks, detect incidents automatically, and initiate actions without direct user intervention.This evolution could fundamentally transform the relationship between individuals, insurers, and risk management systems.What Is Zero-Click Insurance?Zero-Click Insurance refers to insurance systems where policy activation, risk assessment, incident detection, and claim processing occur automatically.Automatic event detectionAI-driven policy managementReal-time risk monitoringAutonomous claims processingInsurance increasingly shifts from reactive service toward continuous background intelligence.What Are Predictive Macro-Claims?Predictive macro-claims are insurance events identified and initiated by large-scale predictive systems before widespread losses occur.Weather-event predictionInfrastructure risk forecastingHealth trend detectionRegional catastrophe intelligenceClaims increasingly become proactive rather than reactive.Why Traditional Insurance Is ChangingConventional insurance systems often involve delays and operational inefficiencies.Manual claims submissionLarge administrative costsDelayed payoutsFraud investigation complexityLimited real-time risk visibilityInsurers increasingly seek continuous risk intelligence.How Zero-Click Insurance WorksAutonomous insurance systems combine real-time data with predictive decision models.Continuous data collectionAI-driven risk evaluationAutomated event verificationInstant claim initiation and settlementInsurance processes become increasingly invisible to customers.Technologies Driving Autonomous InsuranceArtificial intelligenceInternet of Things (IoT)Computer vision systemsPredictive analyticsDigital identity infrastructureSmart contract automationThese technologies collectively create intelligent insurance ecosystems.Examples of Zero-Click InsuranceAutonomous insurance applications may appear across many sectors.Vehicles detecting collisions automaticallyHomes identifying water leakage risksWearables detecting medical emergenciesTravel systems recognizing delays and disruptionsRisk events increasingly trigger automatic responses.Benefits of Predictive Claims SystemsFaster settlementsLower administrative costsReduced fraud exposureImproved customer experiencesEnhanced risk prediction capabilitiesAutomation can significantly improve insurance efficiency.Zero-click insurance transforms insurance from a claim-processing business into a continuous prediction and prevention ecosystem.Traditional Insurance vs Zero-Click InsuranceTraditional → Customer initiates claimsZero-Click → Systems initiate actions automaticallyTraditional → Reactive event processingZero-Click → Continuous predictive monitoringThis changes the operational model of insurance itself.AI and Risk IntelligenceArtificial intelligence increasingly powers insurance decision systems.Behavioral pattern analysisPredictive catastrophe modelingFraud detection systemsAdaptive underwriting modelsAI enables large-scale predictive capabilities.Macro-Risk ForecastingInsurers increasingly monitor broad environmental and economic risks.Climate event predictionDisease outbreak monitoringInfrastructure stress analysisSupply chain disruption forecastingInsurance shifts toward ecosystem-level risk intelligence.Privacy and Ethical ChallengesContinuous monitoring systems raise significant concerns.Data privacy risksBehavioral surveillance concernsAlgorithmic biasConsent and ownership questionsTransparency challengesTrust becomes a critical factor in adoption.Regulatory ConsiderationsInsurance regulators increasingly examine AI-based systems.Automated decision transparencyData governance rulesConsumer protection standardsAlgorithm accountability requirementsRegulatory frameworks continue evolving.Future of Autonomous InsuranceThe future insurance ecosystem may become highly predictive and proactive.AI-native insurance platformsContinuous risk optimizationAutonomous financial protection systemsIntegrated smart ecosystem coverageInsurance may increasingly become invisible infrastructure.Economic and Strategic ImplicationsThe rise of predictive insurance systems could reshape global risk management.Transformation of insurance economicsReduced claims-processing overheadExpansion of insurtech ecosystemsEvolution from compensation toward preventionThis transition could fundamentally redefine the role of insurance in society.Frequently Asked QuestionsWhat is Zero-Click Insurance?An insurance system where AI automatically detects incidents and processes claims without manual user actions.What are Predictive Macro-Claims?Claims initiated using large-scale predictive systems that anticipate risks before losses become widespread.Why is this important?Because it could significantly reduce delays, lower costs, and improve customer experiences through proactive risk management.ConclusionZero-Click Insurance and Predictive Macro-Claims represent a major evolution in the insurance industry where AI, predictive analytics, and connected systems transform insurance from a reactive compensation model into a proactive risk-intelligence platform. While this shift promises improved efficiency and more personalized protection, it also introduces complex questions regarding privacy, governance, trust, and the future balance between automation and human oversight.

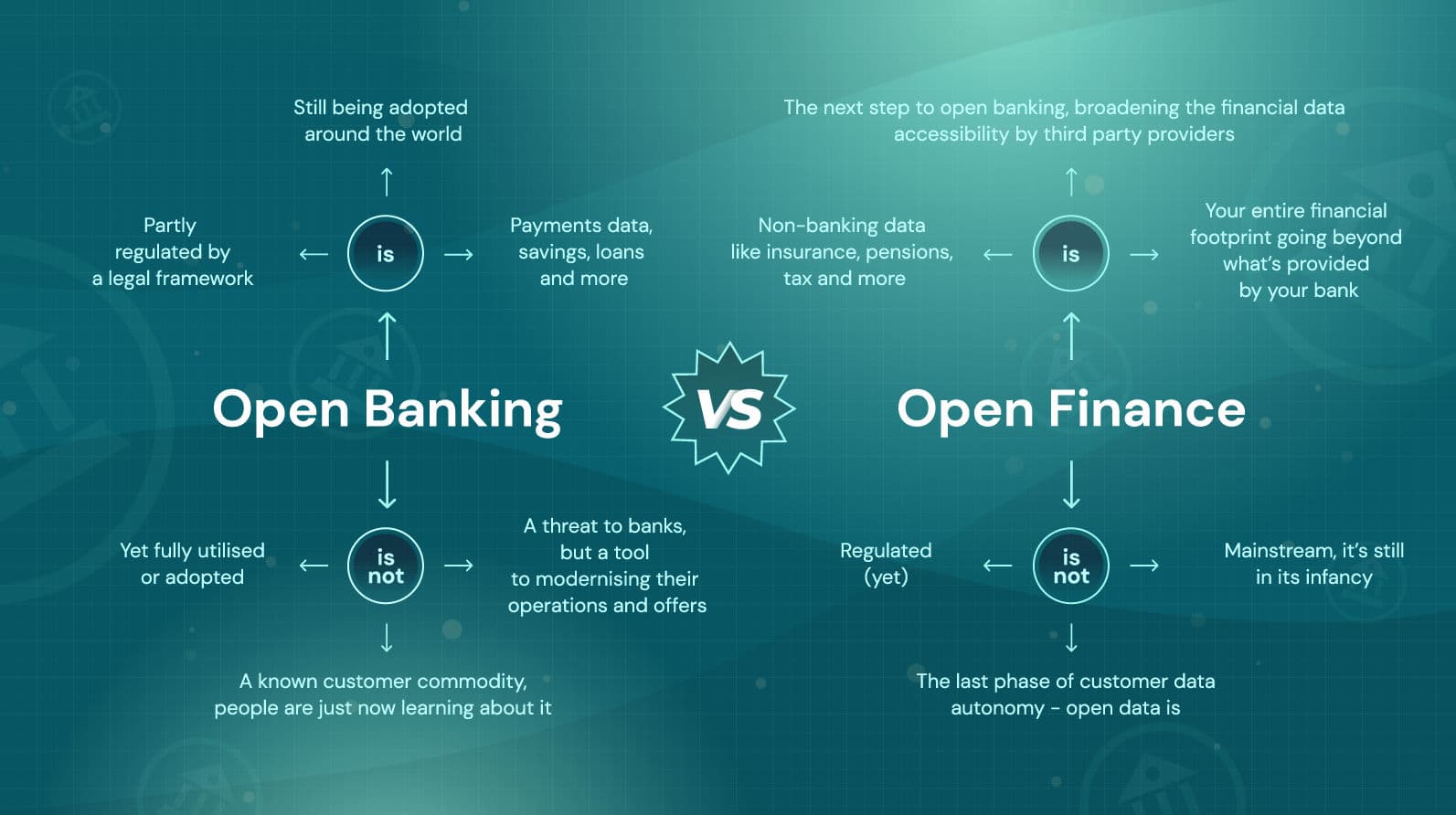

Open Finance vs Open Banking: The Data Super-App Evolution

Open Finance vs. Open Banking (The Data Super-App Evolution)The financial world is rapidly transitioning from isolated banking systems toward interconnected digital ecosystems where data, payments, investments, insurance, identity services, and financial products increasingly operate through integrated platforms. Early digital transformation efforts focused primarily on improving access to banking data through APIs. However, as financial ecosystems evolve, a broader model called Open Finance is emerging.In 2026, the evolution from Open Banking to Open Finance is creating what many describe as the “Data Super-App Era,” where individuals can access and manage nearly every aspect of their financial life through intelligent and interconnected digital ecosystems.This transition could fundamentally reshape banking, consumer behavior, financial competition, and ownership of financial data.What Is Open Banking?Open Banking is a framework that allows banks to securely share customer financial data with authorized third parties through APIs.Bank account data sharingPayment initiation systemsThird-party financial applicationsCustomer-controlled access permissionsThe objective is to improve competition and innovation within banking services.What Is Open Finance?Open Finance extends Open Banking by expanding data sharing beyond traditional bank accounts into broader financial ecosystems.Banking dataInvestment portfoliosInsurance informationRetirement productsCredit and lending systemsDigital assets and payment systemsFinancial information becomes interconnected across multiple services.Why Open Banking Is EvolvingModern financial behavior increasingly spans multiple platforms and services.Multiple financial applicationsDigital investment platformsEmbedded finance systemsCross-platform payment ecosystemsPersonalized financial experiencesConsumers increasingly expect unified financial ecosystems.Open Banking vs Open FinanceOpen BankingOpen FinanceBank account focusedEntire financial ecosystemPayment and account APIsMulti-service data integrationLimited financial scopeComprehensive financial intelligenceOpen Finance expands the reach of data connectivity significantly.The Rise of Data Super-AppsFinancial super-apps integrate multiple services into a unified experience.Payments and transfersInvesting toolsInsurance productsPersonal budgeting systemsLending servicesDigital identity capabilitiesUsers increasingly interact with a single financial interface.AI and Financial PersonalizationArtificial intelligence increasingly powers financial experiences.Personalized recommendationsPredictive spending insightsAdaptive financial planningBehavior-based product suggestionsAI converts connected financial data into actionable intelligence.Benefits of Open FinanceGreater financial transparencyImproved customer experienceEnhanced personalizationExpanded financial inclusionGreater innovation across financial servicesConsumers gain greater control and visibility over their financial activities.Open Banking shares banking data. Open Finance transforms all financial information into a connected intelligence ecosystem.Data Ownership and Consumer ControlFuture financial ecosystems increasingly prioritize user-controlled data access.Permission-based data sharingConsumer ownership modelsGranular privacy controlsConsent management systemsUsers become active managers of financial information.Embedded Finance and Ecosystem IntegrationFinancial services increasingly operate inside non-financial platforms.E-commerce lendingIntegrated insurance servicesSubscription payment systemsContext-based financial recommendationsFinance increasingly becomes invisible infrastructure.Challenges and RisksOpen financial ecosystems introduce several important concerns.Data privacy risksCybersecurity threatsPlatform concentration concernsConsent management complexityRegulatory fragmentationTrust and governance remain essential requirements.Future of Open Financial EcosystemsFinancial systems may increasingly evolve toward intelligent and interconnected platforms.AI-native financial assistantsUnified financial identitiesCross-platform economic ecosystemsAutonomous financial optimization systemsFinancial experiences become increasingly seamless and personalized.Economic and Strategic ImplicationsThe expansion from Open Banking to Open Finance could reshape financial systems globally.Transformation of banking business modelsExpansion of fintech ecosystemsGreater competition among providersShift toward data-driven financial servicesThis transition may redefine the future relationship between consumers, institutions, and financial data.Frequently Asked QuestionsWhat is Open Banking?A system allowing secure sharing of banking information through APIs.What is Open Finance?An expanded ecosystem that includes banking, investments, insurance, lending, and broader financial data.What are financial super-apps?Integrated platforms combining multiple financial services into one unified experience.ConclusionOpen Finance and the evolution beyond Open Banking represent one of the most significant transformations in digital financial systems. By connecting financial data across banking, insurance, investments, payments, and identity ecosystems, the future financial experience increasingly shifts toward AI-powered super-app environments. While this transformation promises greater convenience, personalization, and financial inclusion, it also raises important questions around privacy, governance, and ownership of financial information in an increasingly connected world.

Flexible Credentials and the Payment Card Renaissance

Flexible Credentials & The Payment Card RenaissanceThe payments industry is undergoing a profound transformation driven by digital wallets, embedded finance, artificial intelligence, tokenization, biometric identity systems, and programmable financial infrastructure. Traditional payment cards—once viewed simply as plastic instruments linked to a bank account—are evolving into intelligent financial identities capable of dynamically adapting to context, user preferences, and financial goals.In 2026, a major emerging concept is the rise of “Flexible Credentials” and what many analysts describe as a “Payment Card Renaissance.” Instead of static payment instruments, future credentials may dynamically switch between funding sources, payment rules, identity frameworks, loyalty systems, and programmable financial capabilities.This evolution could fundamentally reshape how people authenticate, pay, borrow, save, and interact with financial systems.What Are Flexible Credentials?Flexible credentials are adaptive payment and identity systems capable of dynamically changing how transactions are processed.Multiple payment source integrationDynamic transaction routingProgrammable payment preferencesIdentity-linked financial functionalityInstead of one fixed payment method, a single credential can support multiple financial functions.Why Traditional Payment Cards Are EvolvingConventional card systems face increasing limitations within modern financial ecosystems.Fixed funding relationshipsLimited personalization capabilitiesFragmented rewards systemsStatic transaction behaviorDependence on legacy payment infrastructureConsumers increasingly expect adaptive and intelligent financial experiences.What Is the Payment Card Renaissance?The payment card renaissance refers to the reinvention of payment credentials from simple transaction tools into programmable financial platforms.AI-powered financial intelligenceContext-aware payment decisionsEmbedded loyalty ecosystemsIntegrated identity servicesPayment cards evolve into intelligent digital financial companions.How Flexible Credentials WorkAdaptive credentials use real-time data and decision systems to determine optimal transaction behavior.Transaction context analysisFunding source optimizationRisk assessment systemsDynamic payment routingFinancial decisions increasingly occur automatically in the background.Examples of Flexible Credential CapabilitiesFuture credentials may automatically adjust payment behavior.Selecting debit versus credit automaticallyOptimizing rewards and loyalty pointsSwitching payment methods by merchant categoryAdjusting spending rules dynamicallyPayment systems become increasingly intelligent and personalized.AI and Adaptive Financial IntelligenceArtificial intelligence is becoming central to payment innovation.Personalized spending recommendationsPredictive financial assistanceFraud detection systemsDynamic financial optimizationAI transforms payment credentials into active financial assistants.Tokenization and SecurityModern payment credentials increasingly rely on token-based security systems.Virtual payment tokensDevice-level transaction credentialsDynamic authentication systemsReduced exposure of sensitive account dataTokenization improves security and privacy.Benefits of Flexible CredentialsGreater personalizationImproved financial efficiencyEnhanced fraud protectionReduced payment frictionIntegrated financial experiencesAdaptive credentials may significantly improve user experiences.Flexible credentials transform payment cards from static financial tools into adaptive digital identities capable of making intelligent financial decisions.Traditional Cards vs Flexible CredentialsTraditional → One card linked to one funding sourceFlexible → Multiple funding and identity layersTraditional → Static transaction behaviorFlexible → Context-aware adaptive decisionsThis changes the role of payment infrastructure.Digital Identity IntegrationFuture payment systems increasingly integrate financial identity capabilities.Biometric authenticationVerified digital credentialsIdentity-based authorization systemsPrivacy-preserving authentication mechanismsPayments and identity become increasingly connected.Embedded Finance EcosystemsPayment credentials increasingly function within broader financial ecosystems.Integrated lending servicesReal-time budgeting toolsEmbedded insurance productsAutomated savings mechanismsFinancial services become integrated directly into payment experiences.Risks and ChallengesFlexible financial systems introduce important challenges.Privacy concernsCybersecurity threatsAlgorithmic decision risksIdentity management complexityRegulatory uncertaintyGovernance and transparency remain essential.Future of Payment CredentialsThe future payment ecosystem may become increasingly intelligent and identity-centric.AI-native payment assistantsAutonomous financial optimizationUnified identity-payment ecosystemsProgrammable financial relationshipsPayment systems increasingly evolve into digital financial platforms.Economic and Strategic ImplicationsThe payment card renaissance could reshape banking and consumer finance.Transformation of payment economicsGreater consumer personalizationExpansion of digital financial ecosystemsRedefinition of financial relationshipsThis evolution may fundamentally alter how individuals interact with money and financial systems.Frequently Asked QuestionsWhat are flexible credentials?Adaptive payment and identity systems capable of dynamically changing payment behavior and funding sources.What is the payment card renaissance?The evolution of payment cards from static transaction tools into intelligent programmable financial platforms.Why are these technologies important?Because they improve personalization, security, efficiency, and integration across financial ecosystems.ConclusionFlexible Credentials and the Payment Card Renaissance represent a major evolution in digital finance where payment instruments become adaptive, intelligent, and deeply integrated with identity and financial services. As AI, embedded finance, tokenization, and digital identity systems continue to mature, payment credentials may evolve from passive transaction tools into active financial decision systems. This transformation could redefine the future relationship between individuals, payments, and the broader financial ecosystem.

Algorithmic Commerce and the Machine-Initiated Economy

Algorithmic Commerce & The Machine-Initiated Economyc Traditional commerce has historically relied on people initiating transactions: consumers browse products, compare prices, place orders, and businesses coordinate supply chains manually. However, advances in artificial intelligence, autonomous agents, connected devices, and digital payment systems are creating a radically different economic model.In 2026, one of the most transformative emerging concepts is the rise of Algorithmic Commerce and the Machine-Initiated Economy — an ecosystem where AI agents, autonomous systems, and connected devices independently discover, negotiate, execute, and optimize economic transactions.This evolution may fundamentally redefine markets, consumption patterns, business operations, and the relationship between humans and economic systems.What Is Algorithmic Commerce?Algorithmic commerce refers to economic activity where software systems and intelligent algorithms participate directly in commercial decision-making and transaction execution.Autonomous purchasing systemsAI-driven transaction executionMachine-to-machine paymentsContinuous optimization of commercial decisionsCommerce increasingly becomes machine-assisted and machine-executed.What Is the Machine-Initiated Economy?The machine-initiated economy describes a system in which intelligent agents and devices independently trigger economic activity.AI agents initiating purchasesAutonomous negotiation systemsSelf-managing supply chainsDevice-to-device financial interactionsMachines evolve from passive tools into active economic participants.Why This Shift Is HappeningSeveral technological developments are accelerating machine-driven commerce.Artificial intelligence advancementInternet of Things expansionReal-time payment systemsAutonomous agent ecosystemsDigital identity and payment infrastructureMachines increasingly possess the information and capabilities required for transactions.How Algorithmic Commerce WorksAutonomous systems continuously analyze needs, prices, preferences, and market conditions.Data collection and contextual analysisDecision optimization algorithmsAutomated negotiation systemsDigital payment executionTransactions occur with minimal human intervention.Examples of Machine-Initiated TransactionsAutonomous economic activity could emerge across multiple sectors.Smart vehicles purchasing charging servicesIndustrial machines ordering replacement partsAI assistants managing subscriptionsSmart homes purchasing supplies automaticallyMachines increasingly become transaction initiators.AI Agents as Economic ParticipantsAI agents increasingly act on behalf of individuals and organizations.Personal commerce agentsEnterprise procurement systemsAutonomous financial assistantsSupply chain optimization agentsAI shifts from advisory systems toward operational actors.Machine-to-Machine PaymentsAutonomous commerce requires new payment systems.Programmable digital currenciesStablecoin payment networksIoT transaction systemsInstant settlement infrastructurePayments become embedded within machines themselves.Benefits of Algorithmic CommerceReduced operational frictionFaster transaction executionContinuous optimization of purchasing decisionsLower transaction costsImproved efficiency across supply chainsAutomation may significantly increase economic productivity.The machine-initiated economy transforms commerce from human-triggered transactions into continuously adaptive interactions among intelligent systems.Traditional Commerce vs Algorithmic CommerceTraditional → Human-initiated transactionsAlgorithmic → Machine-triggered economic activityTraditional → Manual decision processesAlgorithmic → Continuous autonomous optimizationThis changes how markets operate.Role of Digital IdentityAutonomous systems require trusted identity frameworks.Machine authentication systemsDigital ownership credentialsPermission and authorization frameworksIdentity verification infrastructureTrust becomes critical for autonomous economic participation.Risks and ChallengesMachine-driven economies introduce significant concerns.Algorithmic errorsCybersecurity vulnerabilitiesAutonomous fraud risksMarket manipulation concernsLoss of human oversightStrong governance mechanisms remain essential.Regulatory ConsiderationsGovernments and regulators face emerging challenges.Liability and accountability questionsAI governance requirementsMachine identity standardsAutonomous transaction regulationsLegal frameworks must evolve alongside technology.Future of Machine CommerceThe future economy may become increasingly autonomous and interconnected.AI-native marketplacesAutonomous supply chainsContinuous machine negotiationsIntegrated economic intelligence networksEconomic systems may increasingly operate as digital ecosystems.Economic and Strategic ImplicationsThe rise of algorithmic commerce could reshape global economic structures.Transformation of business operationsExpansion of digital economic ecosystemsNew forms of market competitionChanges in consumer behaviorThis transformation may redefine the nature of economic participation itself.Frequently Asked QuestionsWhat is algorithmic commerce?Commerce where intelligent software systems directly participate in commercial decisions and transactions.What is the machine-initiated economy?An economic system where AI agents and connected devices independently initiate transactions and commercial activity.Why is this important?Because autonomous systems may significantly improve efficiency, reduce friction, and reshape how markets function.ConclusionAlgorithmic Commerce and the Machine-Initiated Economy represent a fundamental shift in the future of economic systems. By enabling AI agents, autonomous devices, and machine-to-machine payment infrastructures to independently participate in commerce, this model transforms economic activity from human-centered processes into continuously adaptive digital ecosystems. While this evolution promises major gains in efficiency and automation, it also raises critical questions regarding governance, security, accountability, and the future role of humans within increasingly autonomous economies.

The Stablecoin Interbank Settlement Layer Explained